The problem the survey keeps naming: the roads

When the city asked residents what to fix, the answer was not close. In its recent resident survey, road maintenance and infrastructure was the number-one service respondents said needed the most improvement. 129 named it, more than the next two answers (public safety, 64; community events, 49) combined. Asked separately which transportation improvement would matter most, road repairs and upgrades again came first by a wide margin, 96 responses, against 30 for bike lanes and trails and just 12 for “none, keep taxes low.” See the survey results.

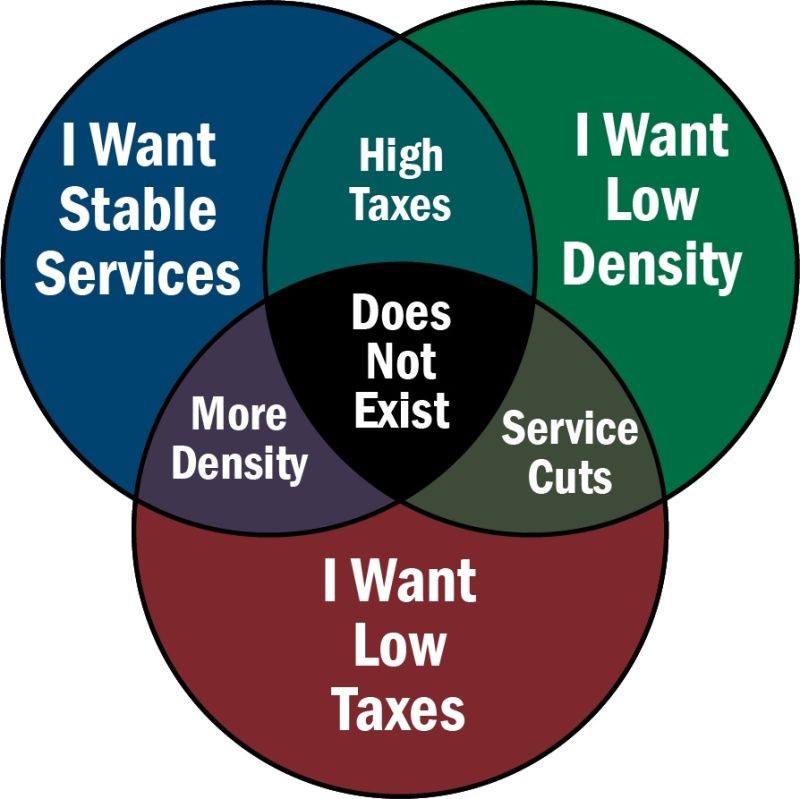

But the same survey asked what new businesses Nowthen needs, and the most common answer was “none, leave it as is” (63), well ahead of the next answer (a grocery store, 14). Only 7 named “anything to help increase our tax base.” The written comments are emphatic in both directions: keep the five-acre minimum, stay rural, keep taxes low, stop developing the farm fields, and also fix the gravel roads.

Those answers pull against one another. Better roads, lower taxes, staying rural, and saying no to most new commercial tax base cannot all win at once. The rest of this article explains why, in dollars, using the city's own records.

This article applies the city tax math to roads. If the mechanics are new to you, start with how your property tax is calculated. The short version: the city rate is the local levy ÷ the local tax base, so growing the tax base lowers the rate, and adding road that the city must plow and repave adds a standing cost the whole town shares.

Compared with every other city in Anoka County, Nowthen has a lot of road for the tax base behind it, and it already spends less to keep that road up than anyone else in the county.

- City road it owns and maintains

- 59 milesMnDOT city-owned centerline

- Tax capacity per city-owned road mile

- $152,000/mi4th lowest of 20 in Anoka County

- Spent per road mile (3-yr avg)

- $15,000/mithe lowest of all 20 · county median $48,000

Nowthen owns about 59 miles of road (MnDOT's count; the city's public-works page lists 61 miles, 25 gravel and 36 blacktop). Behind each mile stands only about $152,000 of tax capacity (the taxable value the city rate is charged on), the 4th lowest of 20. And across the last three audited years the city spent about $15,000 per mile on streets, the lowest of all 20, against a county median near $48,000 and Anoka at about $312,000 a mile. Some of that gap is fair: a rural gravel network is genuinely cheaper to keep up than curbed, lit, storm-sewered city blocks. But it also means there is very little slack. Spending noticeably more on roads can only happen if the city either cuts the budget somewhere else and moves that money to roads, which would keep the levy flat, or raises the levy to pay for a bigger road budget. There is nowhere in our current budget where the city could make cuts deep enough that would make any significant impact on road spending. Raising the levy would result in increased tax rates for all taxpayers unless the tax base widens so that the increased levy spreads over more taxpayers. The tax base only widens with new development. The rest of this article reviews the numbers and math behind different types of development and what impact they would have on the city's tax base. (Spending: MN State Auditor city finances, latest three audited years, operating plus capital. Tax base: DOR payable-2025 taxable net tax capacity. Miles: MnDOT.)

Show all 20 Anoka County cities ▾Hide the table ▴

| City | City-owned miles | Spent / mile (3-yr avg) | Tax capacity / mile |

|---|---|---|---|

| Nowthen (you) | 59 | $15,000 | $152,000 |

| Oak Grove | 125 | $18,000 | $127,000 |

| Ham Lake | 156 | $22,000 | $207,000 |

| Columbus | 71 | $28,000 | $142,000 |

| St. Francis | 49 | $30,000 | $192,000 |

| Spring Lake Park | 27 | $32,000 | $320,000 |

| East Bethel | 131 | $33,000 | $135,000 |

| Bethel | 3 | $38,000 | $196,000 |

| Andover | 206 | $39,000 | $245,000 |

| Lino Lakes | 107 | $45,000 | $335,000 |

| Lexington | 9 | $51,000 | $345,000 |

| Centerville | 16 | $51,000 | $454,000 |

| Fridley | 103 | $53,000 | $397,000 |

| Coon Rapids | 219 | $62,000 | $380,000 |

| Ramsey | 188 | $77,000 | $226,000 |

| Columbia Heights | 57 | $88,000 | $359,000 |

| Blaine | 259 | $101,000 | $448,000 |

| Circle Pines | 17 | $120,000 | $336,000 |

| Hilltop | 1 | $182,000 | $424,000 |

| Anoka | 73 | $312,000 | $315,000 |

Sorted lowest to highest spending per mile. Spending: MN State Auditor city finances, the latest three audited years averaged (operating plus capital street/highway). Miles: MnDOT city-owned centerline mileage, the road each city is financially responsible for, excluding county and state highways. Tax capacity: DOR payable-2025 taxable net tax capacity per city-owned mile. Road types differ: a rural gravel network is genuinely cheaper than curbed, lit, storm-sewered city blocks. Read this as scale, not a report card.

Reading the two columns: tax capacity per mile is how much taxable base stands behind each mile of city road: lower means each mile has fewer tax dollars supporting it. Spending per mile is audited street spending divided by city-owned road miles; it isn't a road-quality score, but it shows the scale of the annual effort next to peer cities.

Why is a road mile so expensive to keep up in the first place? Because the cheap fixes only stay cheap if they happen on schedule. A timely crack seal is a fraction of a reconstruction. The cost ladder, with MnDOT's own per-lane-mile figures, is on the main roads page.

Could the city simply trim the budget to free up that road money? The property-tax page walks through why it cannot move the needle: Can the city just cut the budget? That leaves growing the tax base, which is where the difference between kinds of development starts to matter.

Every new subdivision is more road, forever

The city rate is mostly a story about the tax base. The only real way to raise the levy without raising rates, or to lower everyone's rate while keeping the levy where it is, is to grow the tax base. Not all growth grows the base the same way, though, and the difference begins with the road each kind leaves behind. This is not hypothetical. Almost every residential plat the city has approved added a street the city now owns, plows every snowfall, and repaves every decade or two on its own dime. The clearest evidence is the city's own overlay rotation. Look at whose streets get resurfaced and they are nearly all subdivisions:

- Country Meadows: Eaton Street

- Westphal Country Acres: Argon and Waco Streets

- Morton Farm Preserve subdivision

- Bailey Estates

- Rolling Hills

Names that did not exist as city road until those neighborhoods were built. See the record

Here is the cost side, using only figures the city and state report. Nowthen spends about $7,657 a year maintaining each mile of road (its FY2023 street-maintenance total of $449,328 spread across its ~59 miles). Overlays and reconstruction are extra, and they arrive as big one-time capital projects like the rotation above. On top of the direct maintenance, more road also means more equipment to keep it up, and that costs money too.

Now the benefit side. A rural home brings in about $1,135 a year in city tax (the average Nowthen homestead at the certified 2026 city rate; the tax page shows a little less, about $1,066, for the very same home because it uses the most recent published rate, payable 2025; the city rate ticked up for 2026). That one payment has to cover everything the city does: the sheriff, fire, city hall, parks, and roads. Roads are only about 21% of the budget, so only roughly $244 of that home's tax is actually doing road work. At that rate it takes around 31 homes along a mile of street just to cover its yearly maintenance, before a single overlay.

This very concept was outlined by the city's own planner in a prior project. Reviewing two layouts for the Roessler/Baugh corner in the October 2020 planning packet, the report measured the new street each would require:

- Narrower lots (150-ft minimum): 31 lots on 3,925 ft of road, about 127 ft of street per lot, or roughly 42 homes a mile.

- Wider lots (300-ft minimum): 28 lots on 5,740 ft of road, about 205 ft of street per lot, or roughly 26 homes a mile.

The planner's conclusion, in the city's own words: road length “is directly proportionate to the expected increase in annual City maintenance and future reconstruction costs,” and “wider lots are not likely to generate any additional tax revenue.” Future reconstruction assessments run “1.5X - 2X higher” at the wider width. (Oct 27, 2020 P&Z packet, p.5.)

So a stretch of new city street comes with somewhere between 26 and 42 homes paying toward it, depending on lot size, against the ~31 homes a mile it takes just to cover yearly maintenance, before a single overlay. For scale, one real subdivision overlay, Pinnaker Lake Estates, ran 4,456 feet, about 0.8 of a mile of city road.

In fairness, the city does not bear the whole cost of overlays or reconstruction. When it rebuilds or overlays a subdivision street, Nowthen's practice on these projects is to assess 50% of the cost to the benefitting property owners, with the city covering the other half from the levy. Using the Pinnaker Lake Estates project as an example: that overlay assessed each of the 25 homes about $2,980, paid over roughly 10 years, with the city paying the other 50%. So a homeowner does pay directly toward their own street's reconstruction, which softens the capital side of this. But that split covers those big one-time projects only: the year-in, year-out maintenance, plowing, and dust control, plus the city's own half of every overlay, still come out of the levy the whole town pays. The standing cost a new street adds is real; the assessment just shares part of the reconstruction bill back to the people who live on it.

None of that says a subdivision is good or bad. It is simply the standing cost a new street adds, and how many taxpayers are there to share it. That is the part of the trade the rate hides.

Growing the tax base with commercial development: the corner at 181st and Baugh

Unlike residential development, commercial development concentrates a lot of tax base onto a few acres and does not require the city to add new road it must maintain forever. There is a real example of this in recent city history. It appears here not to second-guess a prior council, but to put real numbers on a real proposed project rather than inventing a hypothetical one. At the corner of 181st Avenue and Baugh Street, in the far southwest of the city with very few neighboring homes, the owners asked to rezone about 41 acres from rural to commercial. The concrete plan on the table was a gas station and liquor store: by the city's own account, Kwik Trip and Bill's Superette had already approached the owner about the corner. Neighbors objected, and the council turned the rezoning down. The corner is still a farm field today. See the record.

That is a perfectly legitimate choice, but it was not free. The cost lands on every Nowthen taxpayer's bill, every year: either a use like that adds to the tax base, or the whole town pays to keep the corner undeveloped. That is the trade, and it is an equation you can put numbers to. What follows is an estimate of that trade-off, and it leans deliberately conservative. The point is not this one project; it is just a way to put a price tag on keeping Nowthen undeveloped. Start with what each acre of that land pays the city in property tax under the different use options (agricultural, residential, commercial):

+-How the tax-per-acre for each kind of land was figuredtap to expand

Every bar above is built the same way: Minnesota turns market value into tax capacity with a class rate, and the city rate is charged on that. The chain for each kind of land, all from figures in the record:

- Farm / rural field: raw Nowthen land has sold for about $2,500–$5,700 an acre (land-sale comps printed in the 2018-07-10 council packet). At the 1% rural-vacant class rate and the payable-2026 city rate of 23.69%, that is about $6–$14 an acre a year.

- Five-acre-lot housing: the average Nowthen homestead has about $4,789 of tax capacity (the official DOR homestead average, roughly 1% of the $480,372 average market value after the homestead exclusion), so it pays about $1,135 in city tax; spread over a 5-acre lot that is roughly $227 an acre.

- Built commercial: instead of guessing, this uses a real comp: the applicant's own two stores in Oak Grove (Bill's Superette, $2,050,600 on 5.85 acres; G-Will Liquors, $1,236,400 on 2.33 acres; Anoka County 2026 assessment). At Minnesota's commercial/industrial class rates (1.5% on the first $150,000 of each parcel's value, 2% above), that is about $7,853 of tax capacity per acre across the 8.18-acre pair, roughly $1,861 an acre a year. A gas-station/store corner sits on a lot of parking and setback, so denser commercial or industrial pays more per acre than this. For scale, a real St. Francis McDonald's ($1,191,500 on 1 acre, same 2026 assessment) works out to about $5,470 an acre, roughly three times the gas station, because a building on a tight lot is the densest tax of all.

One caveat worth stating plainly, because it is the easiest thing to get wrong: the bars show the gross city tax the land itself would pay. The “savings on the average home” figures later in this section are a different, smaller number: they keep only the ~60% local share of new commercial/industrial tax capacity (the other ~40% is shared to the metro fiscal-disparities pool). Gross tax paid by the parcel and rate relief that stays in Nowthen are related, but not identical.

A commercial acre like that pays the city about $1,900 a year, roughly 8 times what an acre of five-acre-lot housing pays, and more than a hundred times an acre of bare field. Now put the corner through that math:

- As it sits today, farmland: the whole 41 acres pays the city only about $550 a year, even at the top of recent Nowthen land-sale prices, a rounding error against the $2,179,043 levy. That is the present reality the rest of these figures are measured against.

- A gas station and liquor store: the use actually on the table. No need to guess what that looks like; just look at the identical pair in Oak Grove. Bill's Superette and G-Will Liquors sit side by side on Viking Blvd, on about 8.18 acres together, assessed by Anoka County at $3,287,000. A corner like that would pay the city about $15,200 a year, roughly what 13 rural homes pay, on eight acres, with no new city road, and it would take only about eight of the corner's 41 acres.

- And a busy corner rarely stops at one use; it clusters. Add a fast-food place and a sit-down restaurant, both of which exist nearby (a St. Francis McDonald's on one acre assessed at $1,191,500; Tasty Pizza Bar & Bowl on 2.2 acres at $742,400) and the corner fills to roughly 11.38 acres and $5,220,900 of value, paying about $24,000 a year, around 21 homes' worth. A small lot holds a lot of tax: that McDonald's alone pays about $5,470 an acre, roughly three times the gas station. This is not a forecast; it is an illustrative clustered-corner scenario built from real commercial comps nearby. A corner like this could draw more than one tenant, but the actual mix would depend on market demand, access, zoning, utilities, and council approvals.

- As housing instead (a hypothetical alternate future, since it is still a field today): the 41 acres as 8 five-acre homes (41 ÷ 5) would bring the city about $9,080 a year, spread across all 41 acres, with new road for the city to plow and repave forever.

Here is why those commercial dollars matter to your bill, and it is the whole point. The city's levy is a fixed pie. It needs to raise $2,179,043 no matter who pays it. For payable 2026 that pie is split across the whole town's tax base at the city rate of 23.69%. Add a commercial taxpayer and it picks up a slice of that same pie, so everyone else's slice gets smaller. The levy does not change; who pays it does.

One wrinkle, kept simple: under Minnesota's fiscal-disparities pool, about 40% of any new commercial tax base is shared out to the wider metro, so only about 60% of it stays in Nowthen to lower your rate. It runs both ways: Nowthen already gets about $153,744 a year back from that pool, roughly $80 off the average home's city bill. But what comes back is set by population, not by how much commercial the city has, so building here would barely change it. The figures below are based only on Nowthen's ~60% share.

- One corner's effect on your rate is real, but small, and that is the honest part. Its $64,200 of new tax capacity, after the ~40% shared to the metro pool, leaves about $39,000 in Nowthen's $9,197,371 base. That nudges the city rate down about 0.10 of a point, roughly $5 a year off the average home. The fuller cluster above takes that to only about $7 a year. A single corner does not slash everyone else's bill dramatically, but it does nudge it down; the thin-tax-base problem is bigger than any one corner.

- Same rate relief, very different long-term cost. Eight five-acre homes add about $38,312 of local tax base. That is almost exactly the same $5-or-so of rate relief as the commercial corner. But the homes do it across all 41 acres and hand the city new road to plow and repave forever, while a commercial corner does it on about eight acres with none. Same nudge to your rate, a fifth of the land, and no standing road bill. That is the whole case for commercial, and it does not depend on the corner ever fully building out.

- Ceiling scenario, not a forecast: even if the entire 41-acre corner somehow reached that same commercial intensity (which no corner does, and never all at once), the most it could shave is about $23 a year off the average home (0.49 points). Treat that as the outer bound, not a prediction.

That is the trade the city made when it kept the corner rural. It is not that farm fields or houses are bad. It is that residential growth adds the most road and the least tax base, so it does almost nothing for everyone else's rate, while commercial concentrates the same tax base on a fraction of the land and asks for no new road.

+-Check the math: every corner figure, worked outtap to expand

Every dollar above comes from the same three steps: market value → tax capacity (Minnesota's class rate), then tax capacity × the payable-2026 city rate of 23.692%. The levy ($2,179,043) and tax base ($9,197,371) are the city's payable-2026 figures. Values are the county's own assessments; only the final figure is rounded.

Farm / rural field

Five-acre-lot housing

Gas station + liquor store (the real Oak Grove corner)

Add two restaurants (the clustered corner)

Ceiling: all 41 acres at that intensity

Two honest notes. Capacity uses each parcel's own first-$150,000 tier at 1.5%, so two parcels get two of those tiers. And the “city tax it pays” figures are gross; the “off the average home” figures keep only the ~60% local share after fiscal disparities, which is why the rate relief is smaller than the tax the parcels pay.

The applicants (Grant Rademacher / Bill's Superette and Kent Roessler), the ~41-acre request, the gas-station / liquor-store use, the motion to deny, and the timeline are from the record (Aug 8, 2017 council minutes; July 25, 2017 P&Z minutes; and the Jan 22, 2019 joint 2040 Comp Plan workshop). The farmland figure is grounded in real Nowthen raw-land sale prices in the record (~$2,500–$5,700 an acre, 2018-07-10 council packet) at Minnesota's 1% rural-land class rate. The commercial figures use a real comp rather than a guess: the applicant's own Oak Grove stores, Bill's Superette ($2,050,600 on 5.85 ac, PIN 29-33-24-14-0016) and G-Will Liquors ($1,236,400 on 2.33 ac, PIN 29-33-24-14-0009), Anoka County 2026 assessment, class 3A commercial, both owned by the Rademacher Family Partnership LLLP. Net tax capacity is figured at Minnesota commercial/industrial class rates (1.5% on the first $150,000of each parcel, 2% above) and the per-acre figure is that capacity over the 8.18-acre pair; denser commercial or industrial would pay more per acre. The clustered-corner figures add two more real Anoka County 2026 comps: a St. Francis McDonald's ($1,191,500 on 1 ac, PIN 31-34-24-41-0018) and Tasty Pizza Bar & Bowl ($742,400 on 2.2 ac, PIN 33-34-24-33-0010), both class 3A commercial. Dollars use the payable-2026 city rate (23.69%), levy ($2,179,043), and tax base ($9,197,371). A full 41-acre commercial build-out is an outer ceiling, not a forecast. Commercial figures apply a simplified fiscal-disparities split (40% of new commercial base to the regional pool, ~60% kept local); Nowthen's payable-2026 area-wide distribution is $153,744.

The road math: what $1,000,000 a year would cost

Put the two halves together. Suppose the city wanted to spend a clean $1,000,000 a year on roads (overlays and reconstruction) funded the only way it can be without a bigger tax base: by adding it to the levy. Run it through rate = levy ÷ tax base:

- $1,000,000 ÷ $9,197,371 of tax base = about 10.9 points added to the city tax rate.

- On the average Nowthen home that is roughly $521 more a year, about 49% on top of the ~$1,066 city share, i.e. close to half again on the city part of the bill.

- Smaller steps scale the same way: every $100,000 of road work funded from the levy is about $52 a year on the average home.

That is the whole bind in one number. The road budget is already lean, so there is nothing to cut your way toward better roads. Which leaves only two honest options: grow the tax base so more properties share the cost, or raise the levy and watch the average bill climb by hundreds of dollars. Those are the practical choices. Try the numbers yourself in the Tax Lab →

Which brings the page back to where it started: the survey. Respondents asked, in the same pages, for better roads, lower taxes, the five-acre rural character kept intact, and no new commercial. Staying rural is a perfectly good goal. It simply is not free. Those four wishes pull against each other, and the arithmetic above is why a city cannot have all four at once: better roads cost hundreds a year on the average bill, the budget is already lean, and the one kind of growth that would quietly pay for roads is the kind respondents most wanted to keep out.

The issue is not really about the few dollars a single corner saves. It is about the pattern. Say no to the gas station, then no to the next commercial corner, then no to the one after, and keep every corner a field, and the result is the thin tax base and the underfunded, lowest-spending-per-mile roads this article opened with. Maybe that is the right trade. But it is a trade, and these are roughly the numbers. And if that corner was not the right place for commercial, what place is? These opportunities are not just there for the taking. They need a willing landowner, a real operator ready to move on a real project, and a busy enough location to support the business, and those things rarely line up, certainly not on demand.

Before saying no to any development at all, as most respondents in the survey did, it is worth seeing the price first. Keeping rural corners rural may well be the right choice, but it is a choice, and it should be made with the price visible. Less commercial tax base means fewer dollars sharing the cost of the roads everyone uses. The question is not whether rural character matters; it plainly does. The question is how residents want to pay for it. Next time you drive by that intersection, look at that empty field and ask what that rural choice is worth on the tax bill.

Want to test the tradeoff yourself? The Tax Lab on the property-tax page lets you raise or cut the levy, add a road program, or grow different kinds of tax base, and watch the average bill move in real time.